Plan Smarter. Grow Stronger. Don’t miss our latest financial strategies.

May 2, 2026

Cash-Out Refinance vs HELOC: Which Is Actually Better in 2026?

You've built real equity in your Florida home. You need cash. But you also locked in a great rate years ago and you don't want to blow it up. Here's the honest answer — without the call-center pitch.

You're sitting on six figures of equity. Your kitchen is from 2003, the roof is cracked from the last hurricane season, the credit cards are creeping up...and yet, every time you think about touching your mortgage, your stomach tightens. You refinanced in 2021 at 2.875%. Giving that up feels insane.

So you're stuck. And in 2026, with rates still hovering well above where you locked, almost every Florida homeowner I talk to is stuck in the same place. The good news: you usually don't have to give up that rate to access your equity. Let's break this down simply.

The 30-second answer

If your current mortgage rate is below ~5% and you need cash, a HELOC almost always wins in 2026. If your rate is already at or above today's market and you need a large lump sum (60k+), a cash-out refinance usually makes more sense. Most other situations fall somewhere in between — and that's where talking to a real person matters.

What is a cash-out refinance?

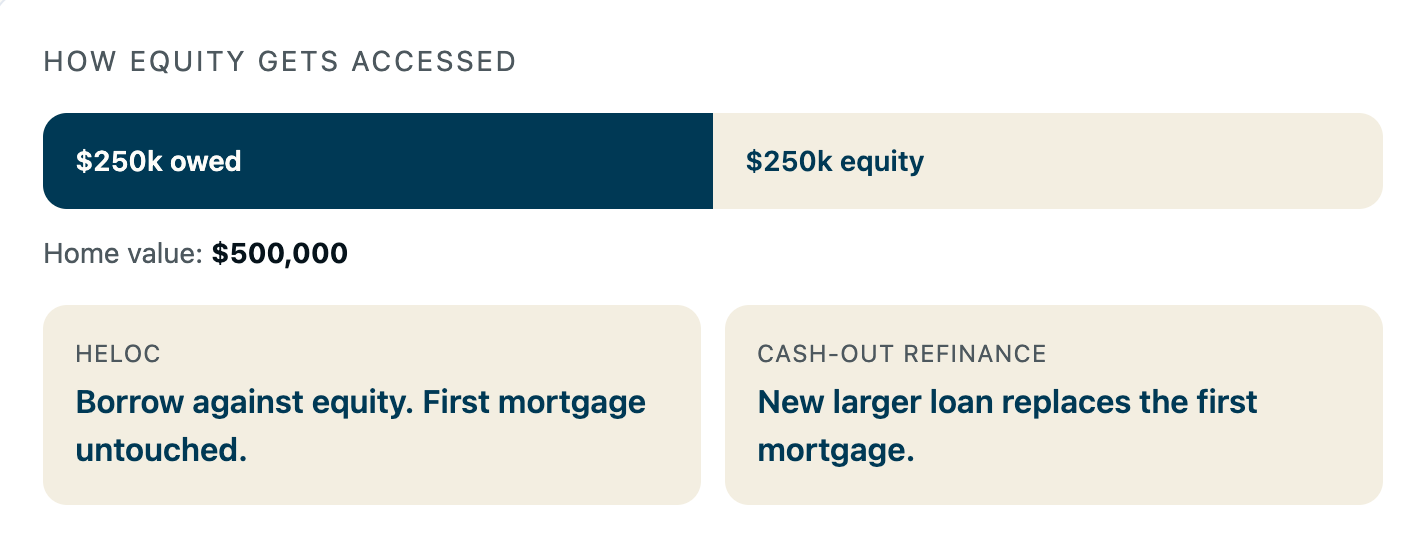

A cash-out refinance replaces your existing mortgage with a brand-new, larger one. You pocket the difference in cash. If you owe $250,000 on a home worth $500,000, you might refinance into a $350,000 loan and walk away with $100,000 (minus closing costs).

The catch: your entire mortgage gets repriced at today's rate. According to the Consumer Financial Protection Bureau, this is why cash-out refis stopped making sense for most homeowners after 2022 — you're trading a low rate for a higher one across your whole balance.

What is a HELOC?

A Home Equity Line of Credit is a second loan that sits behind your first mortgage. You don't touch your existing loan at all. Instead, you get a credit line — think of it like a credit card backed by your home — and you only pay interest on what you actually draw.

HELOC rates are variable and tied to the Prime Rate (set in response to Federal Reserve policy). In 2026, most qualified Florida borrowers are seeing HELOC rates in the 8–10% APR range. That sounds high — until you realize you're keeping your 2.875% on the other $250k.

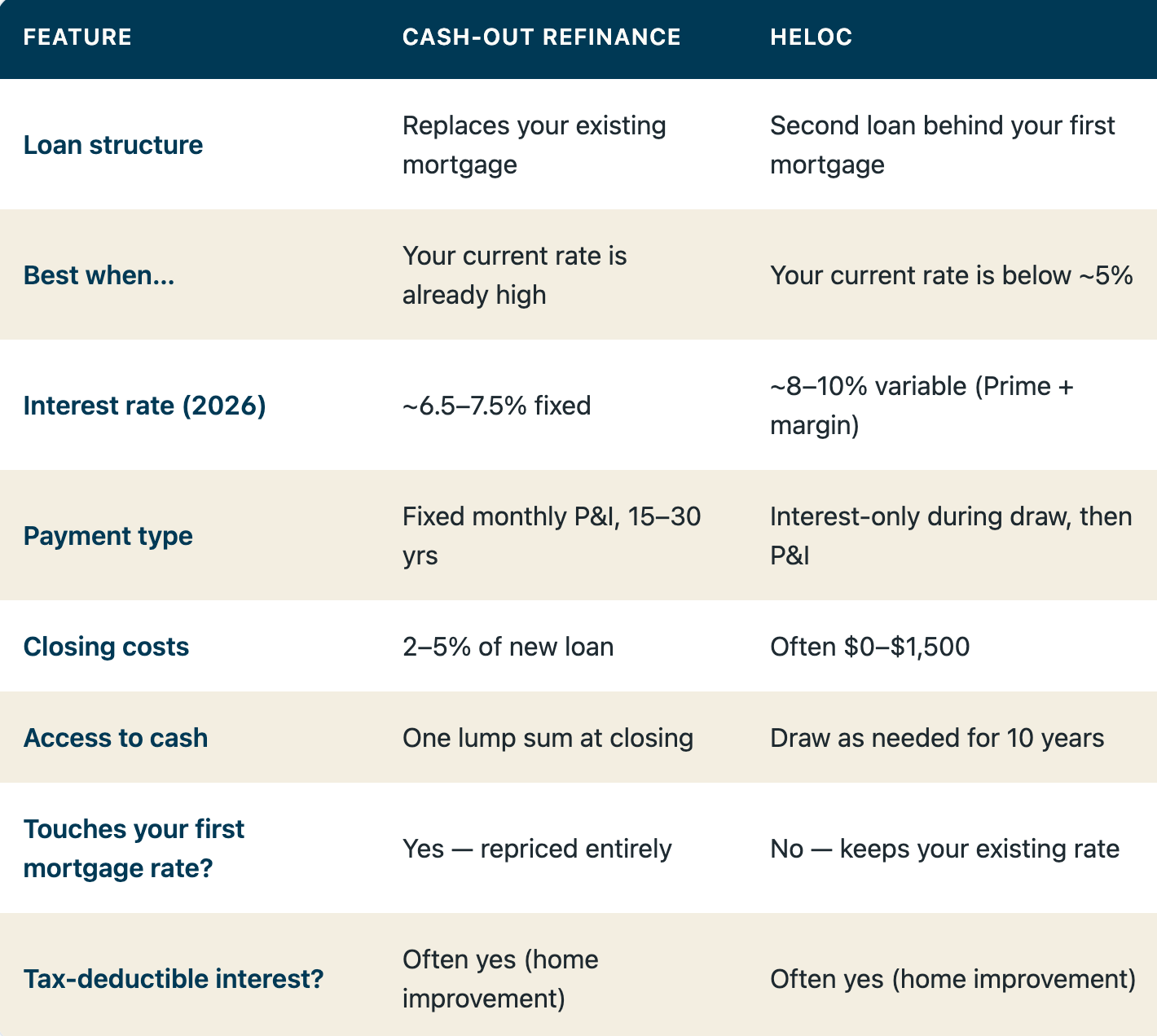

HELOC vs Cash-Out Refinance: Side by side

Here’s a side-by-side breakdown of how a cash-out refinance compares to a HELOC across structure, rates, and flexibility:

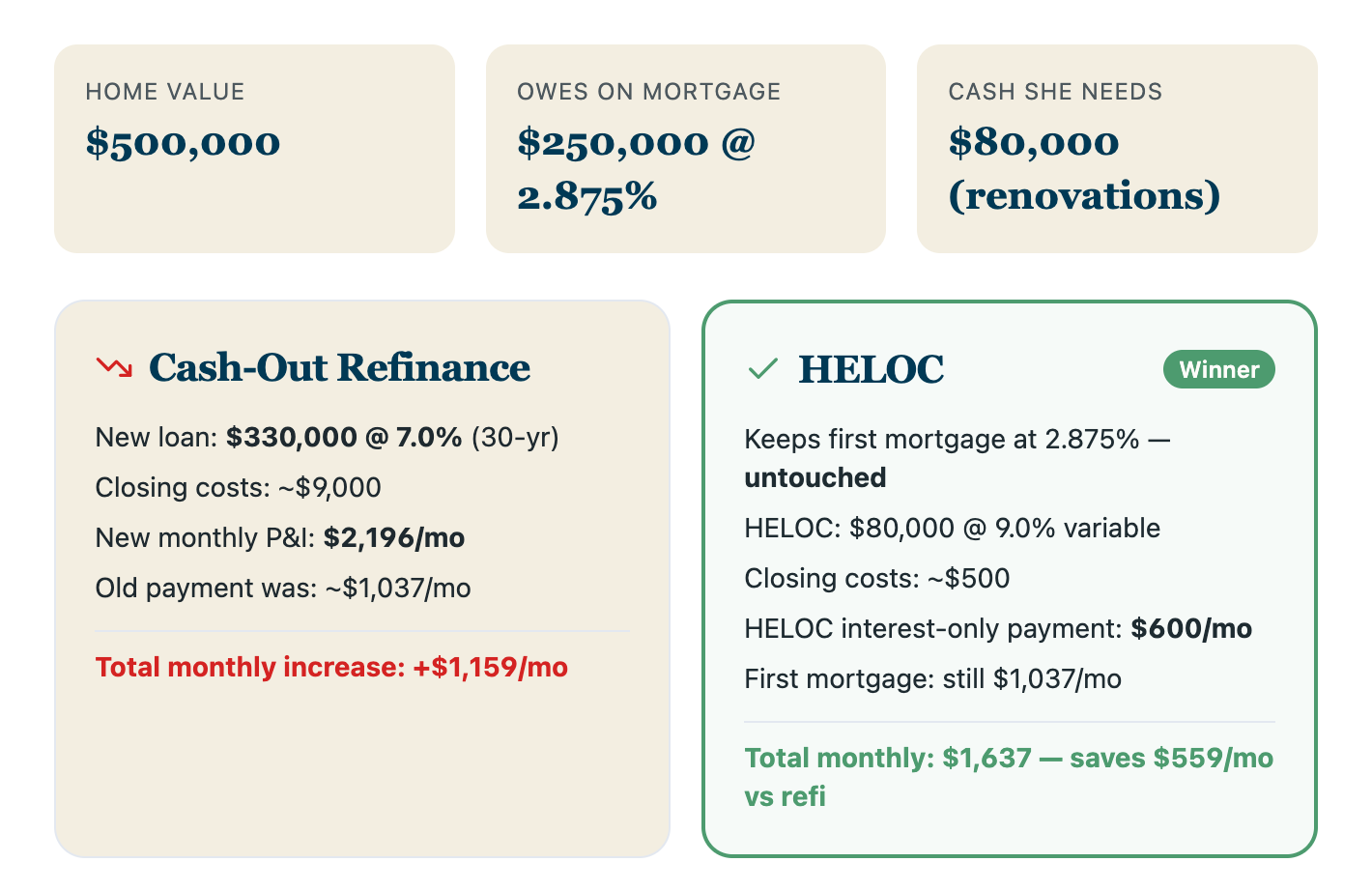

A real Florida scenario (with numbers)

Let's run the math on a typical Tampa homeowner — call her Maria. Same situation I see weekly:

Look at that gap. Maria's total monthly payment is $1,028/mo lower with the HELOC, even though the HELOC's interest rate is more than double her first mortgage. Why? Because she's not repricing the $250k she already owes at 2.875%. That's the whole game in 2026.

When a HELOC makes more sense

When a cash-out refinance makes more sense

When neither is a good idea

Be honest with yourself

Tapping home equity is borrowing against the roof over your head. Don't do it for:

Florida-specific considerations

Florida isn't like everywhere else. A few things change the math here:

Homeowners insurance is brutal

Premiums in Florida have climbed 40%+ since 2021. Lenders escrow this — bigger premium = bigger monthly payment. Refinancing reshuffles your escrow and you may owe a lump-sum cushion at closing.

Hurricane risk affects appraisals

Post-storm appraisals can come in lower than expected. Lock your appraisal early in hurricane season (June–November) when possible.

Homestead exemption stays

Both HELOCs and cash-out refis keep your homestead exemption intact. You don't lose Save Our Homes protection.

No state income tax = stronger DTI

Florida's no-state-income-tax means your take-home is higher than the same salary in NY or CA — which often helps you qualify for more.

Estimate Your Home Equity Options

Run the quick numbers in your head:

Check Zillow and take 5% off to be safe

Look at your last mortgage statement

Do not round up. Borrow only what you need.

If line 1 minus line 2 is more than 1.25x line 3, you almost certainly qualify. The next question is not can you. It is which option. That is where 30 minutes with Tim can save you years of overpaying.

Common mistakes Florida homeowners make

Refinancing the whole mortgage just to grab $40k. If you have a sub-5% first, a HELOC is almost always cheaper. Don't let a loan officer talk you into a full refi for a small cash need.

Consolidating credit cards, then running them back up. This is the #1 reason people lose their homes after a cash-out. If you do this, freeze the cards. Literally.

Maxing out the HELOC because it's "available." A HELOC is a tool, not a savings account. Borrow what you need and start paying it down.

Ignoring closing costs. A cash-out refi can run 2–5% in closing costs. On a $350k loan, that's $7k–$17k. HELOCs typically have lower or zero closing costs — another reason they win for smaller needs.

Going with the first lender that calls back. Fannie Mae and Freddie Mac back most of these loans, but pricing varies wildly by lender. Get at least two real quotes.

Why homeowners talk to Tim, not a call center

Tim at Miller Home Loans isn't a 1-800 rep reading from a script. He's a Florida-based broker who walks you through both options honestly — even when the answer is "don't refinance, get a HELOC instead" (which means a smaller commission for him). Because Miller works with Edge Home Finance, Tim has access to dozens of lenders and can shop your loan instead of pushing one product.

Frequently asked questions

Is a HELOC or cash-out refinance better in 2026?

What are HELOC rates in Florida right now?

How much equity can I borrow from my home?

What are HELOC requirements in Florida?

Can I use a cash-out refinance for debt consolidation?

Will refinancing in Florida cost me my homestead exemption?

The Bottom Line

In 2026, most Florida homeowners shouldn't touch their first mortgage. If you locked in a great rate, protect it. Use a HELOC for flexible access, a cash-out refi only when the full math actually works in your favor. Don't let anyone — including your bank — push you into the wrong product because it's easier for them to sell.The right move is rarely the loudest one. It's the one that fits your rate, your equity, and your life over the next 5–10 years. That's the conversation worth having.

See what option makes the most sense for your situation

No pressure, no call center. Just a real conversation with Tim about your actual numbers.

Work Directly With Your Loan Expert

Skip the call centers and talk directly to an expert who handles your loan from start to finish.

Email Address:

Tim@Millerloans.com.svg)

Phone Number:

(407) 404-3834Proudly Serving Homebuyers Across Florida and Pennsylvania, including: Orlando • Tampa • Miami • Jacksonville • Philadelphia • Pittsburgh • Allentown

Miller Home Loans is a marketing name for Tim Miller (NMLS #2220372), a licensed mortgage loan originator with Edge Home Finance, LLC (NMLS #891464). Edge Home Finance, LLC is an Equal Housing Opportunity mortgage broker. All loans are subject to credit approval. This is not a commitment to lend. Terms and conditions apply.

Licensed in FL and PA. For licensing information, please visit www.nmlsconsumeraccess.org